Subscribe to Our Newsletters

National Hog Farmer is the source for hog production, management and market news

February 24, 2014

There are a number of news items of value today and they have some broad implications.

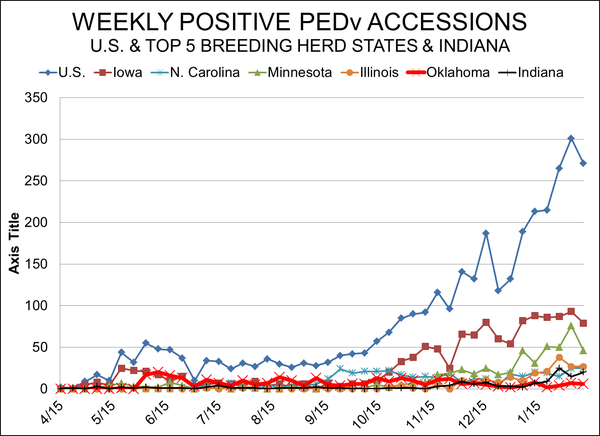

First, the number of porcine epidemic diarrhea virus (PEDV) case accessions at veterinary diagnostic labs fell for the week of February 10. (See Figure 1 in this story). Furthermore, the decline was the largest on record outside of the sharp drop at Christmas. Those are the good news items. The bad news is that the 30-case decline was from the all-time record high of 301 accessions the week of February 3, and that one point does not make a trend. But in this fight, we’ll take all of the good news we can get.

Figure 1

In addition, there is news out of Canada that point-to-plasma products are being discussed as a possible transmission vector for PEDV. The results are still sketchy to this social scientist, but I do know that U.S. companies had thoroughly investigated plasma as a disease-spreading agent several months ago, so I’m not too sure what to make of the Canadian findings at this point.

One thing is certain, though: supply impacts will get larger. That is, based on the chart, pretty much a no-brainer but the magnitude is pretty shocking. Only 3.5% of the total accessions to-date occurred in August 2013 and would thus be impacting February 2014 slaughter. Compare that figure to this: 25% of the to-date accessions occurred in January and will impact July slaughter. “But these aren’t just baby pig cases,” you say. And you are correct. If I use just the suckling pig data from the National Animal Health Laboratory Network’s weekly report, though, the percentages are 9.4% for August and 30.9% for January. So, whatever the impacts on February slaughter, I would expect them to be at least 3 times as large in July. Those $105-plus futures – and even higher – may well be justified.

Second, USDA’s Cattle On Feed Report indicates, as expected, that cattle supplies will remain very tight in the short run and tight through early summer. The number of cattle in U.S. feedlots with capacities of 1,000 head and more, was 10.76 million head on February 1, which was 2.8% lower than one year ago. The decline was a bit smaller than the expected 4% figure, though, so that news may be a bit bearish for cattle futures.

Like what you’re reading? Subscribe to the National Hog Farmer Weekly Preview newsletter and get the latest news delivered right to your inbox every week!

January placements were 8.6% higher than last year and much higher than the 2.8% increase that was expected by analysts. This suggests that some of the supply crunch may ease come July. Until then, cattle and beef prices will remain at or beyond record levels, providing some strong substitution opportunities for pork.

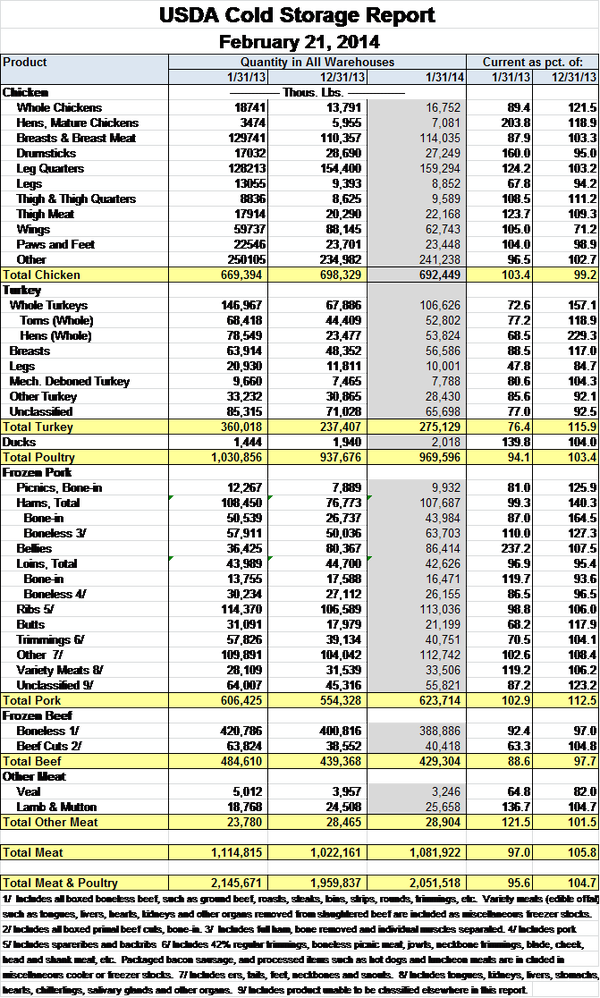

USDA’s Cold Storage report, however, shows that there is more pork in freezers as of the end of January. See Table 1. Total pork stocks were 2.9% higher than one year ago and 12.5% higher than at the end of December. Pork bellies accounted for all of the year-on-year increase, growing by nearly 50 million pounds or 127%. We view these stocks as a hedge on the part of bacon producers against another run-up in belly prices this summer. That is not to say that bellies or bacon will be cheap, but users want to make sure they don’t have to go to spot markets to fill their needs. Without a bellies futures contract, holding inventory is about the only way to hedge against seasonally higher prices.

Table 1

Higher ham stocks accounted for over 40% of the month-to-month increase in pork inventories. Part of that is seasonal storage for Easter, which falls on April 20, a relatively late date, this year.

Beef supplies are relatively tight, especially in light of the slaughter levels we are likely to see with lower feedlot inventories and ongoing efforts to build the beef cow herd. Broiler breast inventories continue to shrink relative to last year but leg quarter product stocks are sharply higher at +26% from February 2013 and +19% from the end of December

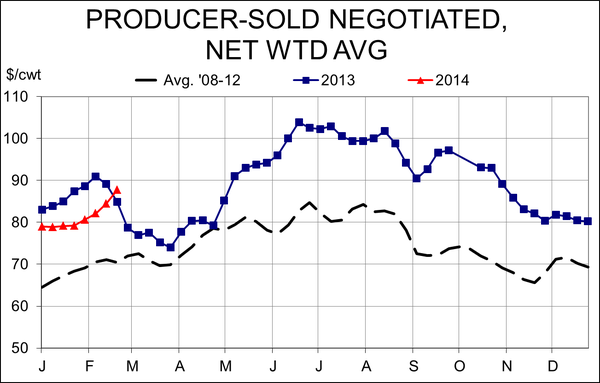

Weekly cash hog prices have risen above year-ago levels (See Figure 2) for the first time this year. The year-on-year comparisons will get very large over the next few weeks because we will be comparing this year’s strong prices to ones that were negatively impacted by last spring’s exit from the U.S. market by Russia and the uncertainties created by China’s vague ractopamine “certification” demands. Seasonally lower hog supplies will make the differences even greater.

Figure 2

History says that hog prices rise about $15/cwt. carcass from mid-February to summer highs. That would put this year’s peaks in the $103 range, well below the record levels of lean hogs futures last week. The market is clearly factoring in a greater-than-normal seasonal reduction in supplies based on PEDV. Whether it is large enough remains to be seen.

You might also like these stories:

How Long Can PEDV Survive in the Environment

Sow Housing Comparison: Consulting the Data

Will Shrinking Consumer Disposable Income Threaten Pork Demand?

You May Also Like

Enter a zip code to see the weather conditions for a different location.