Subscribe to Our Newsletters

National Hog Farmer is the source for hog production, management and market news

January 13, 2014

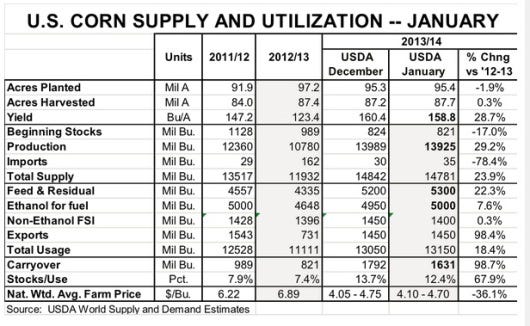

Friday’s World Agricultural Supply and Demand Estimates (WASDE) Report from USDA surprised the trade a bit with a reduction of the estimated U.S. average yield. Analysts had expected USDA to raise the yield to 163.3 bushels per acre from December’s figure of 160.4 bu./acre but USDA dropped the yield to 158.8 bu./acre (See Table 1). That decline was partially offset by a 500,000-acre increase in harvested acres, leaving the 2013 crop estimated at a still record-large 13.925 billion bushels. That is nearly 30% larger than last year.

USDA also increased total usage by 100 million bushels by adding 100 million to feed/residual and 50 million to ethanol, while dropping non-ethanol food, seed and industrial usage by 50 million bushels. The curious one there is the increase to the feed/residual usage which, now at 5.3 billion bushels, is over 22% larger than last year. This latest 100-million bushel increase for corn feed/residual use is accompanied by a 60-million bushel reduction in wheat feeding. That explains some of the number. But the net increase in feed/residual usage for all feedgrains (corn, sorghum, barley and oats) and wheat now stands at 852 million bushels or 17%.

Table 1:

Chicken numbers will grow this year by 3-5%. Cattle numbers will be down sharply but lower-cost corn could play a bigger role in finishing rations. Hog numbers were expected to grow, but porcine epidemic diarrhea virus (PEDV) losses have put a big dent in those plans, even though the 100 million or so pigs that will come to market will likely be 2-3% heavier than they would have been without the PEDV losses.

How does that small increase in livestock numbers amount to a 17% increase in feed usage? We don’t think it does, and we are somewhat concerned about the computations if a number that large is attributed to “residual.” As one of our friends pointed out, “residual” appears to be a euphemism for “I don’t know.” We understand USDA can’t be too precise on this number, but lumping it with feed causes some difficulties when one is trying to gauge feed usage against livestock and poultry numbers.

Keep the most in-depth pork production information available at your fingertips! Download our Blueprint app today.

The bottom line is that corn will be a bit more expensive, but not much. The mid-point of USDA’s forecast price range remained $4.45/bu. CME Group futures rallied by $0.15-$0.20 /bushel on Friday, were steady over the weekend and have seen small gains today.

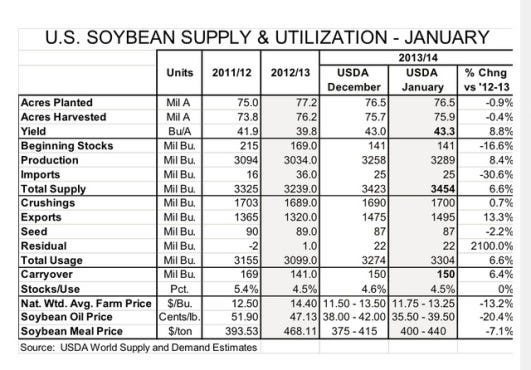

USDA’s forecasts of soybean supply and demand were about as expected. They increased the yield and harvested acres slightly, but increased crush and exports to offset the changes, leaving forecast year-end stocks at 150 million bushels, 4.5% of total usage (See Table 2). That is the same stocks/use ratio as last year (and 2009 and 2010) and the second- lowest on record. USDA increased the South American crop slightly, but suffice it to say that soybean supplies will still be tight when U.S. planting season rolls around.

Table 2:

The really bad news for hog producers is that USDA thinks soybean meal will be forced to carry even more of the soybean value proposition. They lowered their forecast price for soybean oil by $2.50/cwt. to $35.50 - $39.50 and increase the forecast meal price to $400.00 - $455.00 per ton.

What does this mean for costs? My model, which is based on Iowa State University’s Estimated Costs and Returns series, says average costs went up by about $1.10 from Friday to Monday. The average, as suggested by futures prices at mid-session Monday, is $78.53/cwt. carcass. That still compares very favorably to the averages of the past two years, $90.89 and $93.91.

The cost increase and a slight downtrend in Lean Hogs futures leaves our model’s profit outlook for 2014 at $24.86 per head, about $2.50/head lower than last week but still quite good. That profit level would put 2014 roughly equal to 2005 and still with a chance to be the best year for U.S. pork producers since 1990.

Friday’s report altered the outlook slightly but not materially. I still expect 2014 to be a banner year for pork producers – and even a good year for those who suffer PEDV losses.

You might also like:

2014 Looks Good for U.S. Pork Producers

Pace of PEDV Cases on the Rise

You May Also Like

Enter a zip code to see the weather conditions for a different location.