thumbnail

Farming Business ManagementPork production software aids in difficult decision makingPork production software aids in difficult decision making

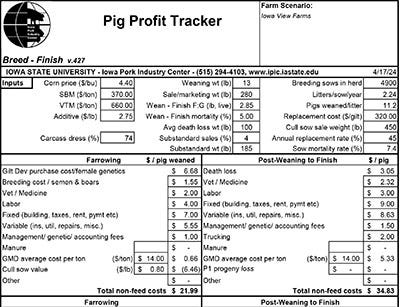

Pig Profit Tracker can help producers assess value, performance changes within their operation.

.jpg?width=300&auto=webp&quality=80&disable=upscale)

Recent Headlines

Enter a zip code to see the weather conditions for a different location.

Sep 27, 2023

Sep 27, 2023

Global Hog Industry Virtual Conference

Subscribe to Our Newsletters

National Hog Farmer is the source for hog production, management and market news