Subscribe to Our Newsletters

National Hog Farmer is the source for hog production, management and market news

Last week’s Crop Production and World Agricultural Supply and Demand Estimates (WASDE) reports provided some much-needed good news for livestock and poultry production costs going into the 2012-13 crop year. The WASDE contained USDA’s first official estimates of the coming crops and potential usage of those supplies.

May 14, 2012

Last week’s Crop Production and World Agricultural Supply and Demand Estimates (WASDE) reports provided some much-needed good news for livestock and poultry production costs going into the 2012-13 crop year. The WASDE contained USDA’s first official estimates of the coming crops and potential usage of those supplies.

While hog and cattle prices have been disappointing of late, the projected record corn crop may go far to keep some of these margins in the black next year.

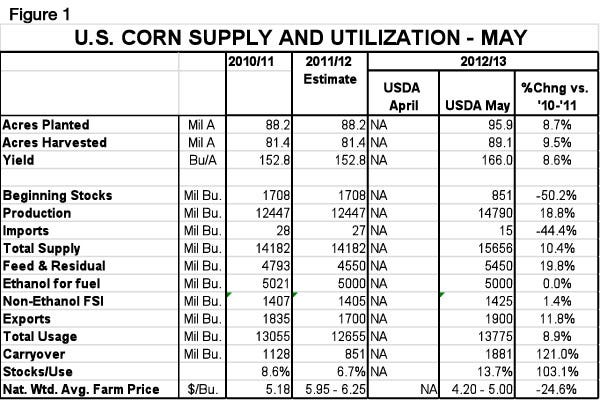

USDA assumed that March’s planting intentions of 95.9 million acres would come to fruition when final plantings are estimated in June. We think that is reasonable given the extraordinary rally in the soybean complex to compete for acres during May and June. Our initial thought was that the unusually early start to corn planting may actually result in more corn acres, but a slowdown in progress over the past couple of weeks and the fact that soybeans are now offering higher returns than most corn-on-corn scenarios might turn the acreage totals the other way. A stand-off between rapid progress and the rally in soybean prices seems reasonable at this juncture.

USDA’s assumed yield of 166 bu./acre would break the existing national average yield record of 164.7 set in 2009, which is 2.4 bushels above the 1996-2000 trend yield of 163.6 bu./acre. The USDA projection is 7 bu./acre above the 1960-2011 trend yield of 157.3 bu./acre.

All considered, the weather will have to be about perfect to get to 166 bu./acre for the national average yield. Early planting almost eliminates frost concerns this fall, but with nearly 96 million acres being planted, a good number of non-optimal acres will have to yield exceptionally well. Recent rains in northern Iowa and southern Minnesota have improved moisture conditions there, but temperatures and rainfall will have to be “just so” for this yield to materialize.

If it does, though, we will have nearly 15 billion bushels of corn from which to draw 2012-13 usage. USDA says ethanol usage will not increase in 2012-13 – and I tend to agree. Ethanol output already exceeds the Renewable Fuel Standard for the coming year. Ethanol margins are small or negative and the nation’s fuel supply is already saturated with ethanol at the 10% inclusion rate. Add in the slow to non-existent uptake of E15 and there just won’t be any growth in ethanol usage this year.

Lower-priced corn will almost surely push exports higher even with ample world wheat supplies. We think USDA’s 200 million bushel increase in exports is reasonable.

But we have no idea where U.S. livestock, poultry and dairy operations are going to use 900 million more bushels of corn. That’s nearly 20% of this year’s projected feed and residual usage and there will be fewer cattle on feed and fewer dairy cows. Hog numbers could grow by 1% or so and chicken numbers will likely grow by 1-3%, but a 20% increase in feed usage seems unlikely.

Perhaps it is the residual component. When USDA reduced feed and residual usage this year, they once implied that higher priced corn would reduce waste. Maybe we will reverse that logic and waste more of “cheap” $4.20-to-$5.00/bu. corn. I’m being facetious about USDA’s comments and wastage – but we must always remember that this line of the corn supply and utilization table includes all of the errors in all of the other lines.

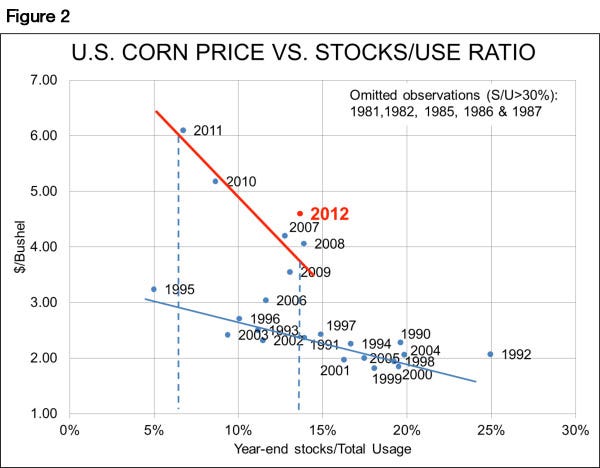

USDA’s estimated average farm price now stands at $4.20 to $5.00/bu. for 2012-13. As Figure 2 shows, the mid-point of that range ($4.60) is higher than recent years’ price vs. stock/use ratio relationship would suggest. Could the season-average price be below $4.00/bu.? We doubt that, but something in the low $4.00 range is entirely possible should those yield levels be reached.

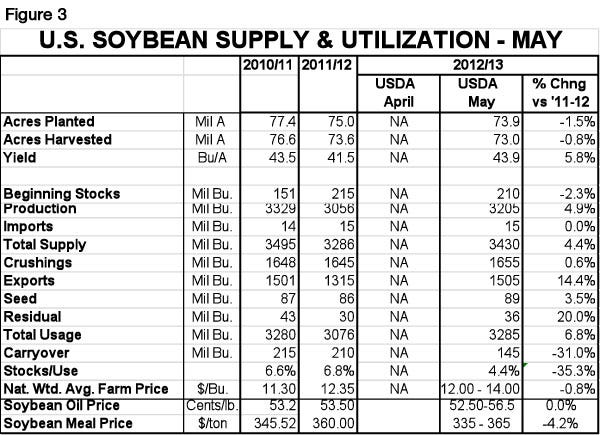

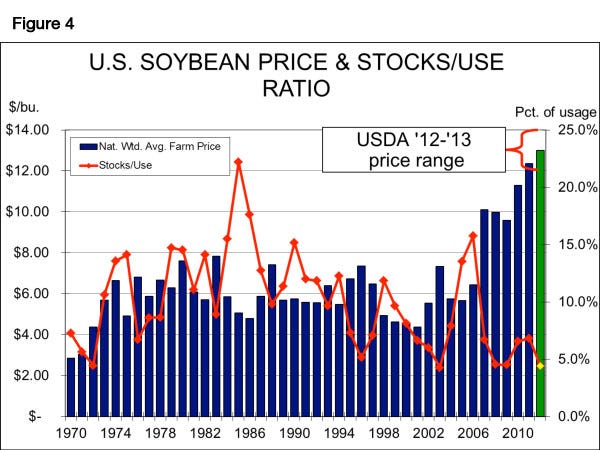

The report, though, was quick to take away at least part of what it bestowed. The projected 2012-13 soybean balance sheet (Figure 3) was as tight as the corn sheet was loose. Even a near-record yield of 43.9 bu./acre (up nearly 6% from last year) left projected year-end carryout stocks at only 145 million bushels, 31% lower than last year and the fourth lowest since 1972. The projected year-end stock-to-use ratio is 4.4%, the lowest on record, represents just 2.3 weeks’ worth of supply at year’s end (Figure 4). According to USDA, it would also result in the highest average soybean price ever – about $13/bu.

What does this mean for pork producers? If the midpoint of USDA’s projected ranges for corn ($4.60) and soybean meal ($350/ton) occur, the Iowa State University model for costs for an average Iowa farrow-to-finish operation would put costs at just over $76/cwt., carcass, or about $57/cwt. on a live weight basis. That compares to $86.15/cwt., carcass, for this year and $86.70/cwt. for last year.

Two things could happen. Hog producers could hold the line on numbers and enjoy a reasonably profitable 2013 due to costs that are roughly $20/head lower. Or, they could see these lower costs as a reason to expand and, thus, push prices lower by late-2013. My guess is the latter will occur to some degree.

But remember that more corn and more soybeans in no way mean more slaughter capacity – the most critical limiting factor to U.S. pork output for the next two years.

You May Also Like

Enter a zip code to see the weather conditions for a different location.