Subscribe to Our Newsletters

National Hog Farmer is the source for hog production, management and market news

Happy New Year! Regardless of the challenges that loom on the horizon, in the New Year we all see a clean slate upon which much will be written. More important, most feel some degree of control and power over the letters that will be inscribed over the next 12 months.

January 7, 2013

Happy New Year! Regardless of the challenges that loom on the horizon, in the New Year we all see a clean slate upon which much will be written. More important, most feel some degree of control and power over the letters that will be inscribed over the next 12 months. Whether such dominion over our own fortunes and the fortunes of those for which we care is true this year remains to be seen. But hope, good wishes and high expectations spring eternal. As evidence, I offer the Chicago Cubs baseball team – the World Champions in 1908 – will begin spring training soon. Perhaps 2013 will indeed be their year!

So what do I think will be the key questions for the pork industry in 2013? Here is my A-list:

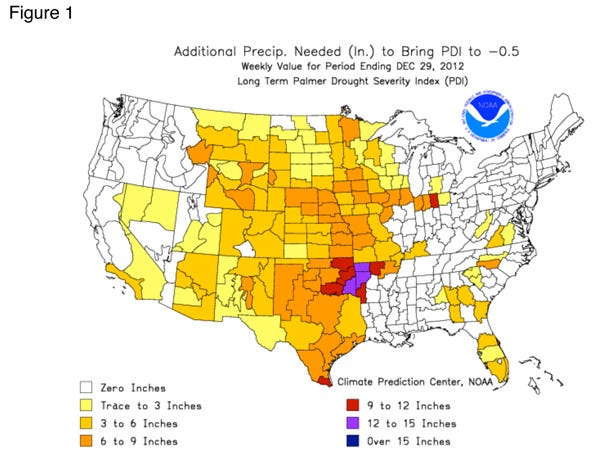

Will it rain? Where will it rain? When will it rain? How much will it rain? Okay, that’s four questions, but they are all important and they center on an obvious theme. The National Weather Service map (Figure 1) indicates that conditions are improving in the Corn Belt, but 6-9 in. of rain are still needed in many areas from northern Illinois through Nebraska and Kansas to get us back to normal for the Palmer Drought Index. Things aren’t great, but it’s much better than last fall when some areas needed 12 in. or more. I seriously doubt that we will get enough snow to get back to normal before spring. But 6-9 in. is possible and timely rains during the growing season will produce a crop even if subsoil moisture is short. We were in much this same predicament last year – though not as severe – so everyone knows this is no slam dunk. One warning, though: There may not be much hard red wheat available next summer to stretch feed supplies. Things are very bad in Texas, Oklahoma and much of Kansas. They will need, at worst, normal winter temperatures and then very timely rains this spring to get a reasonable harvest this summer.

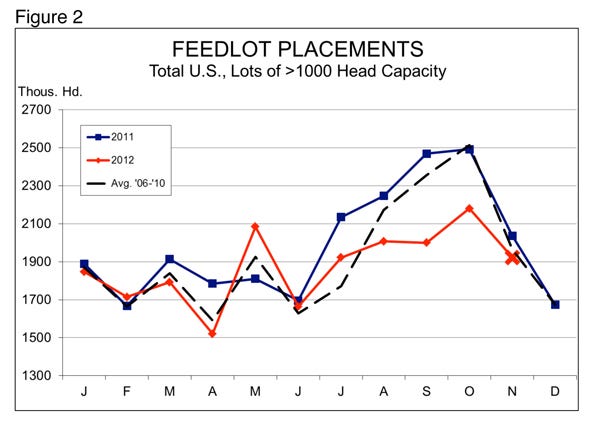

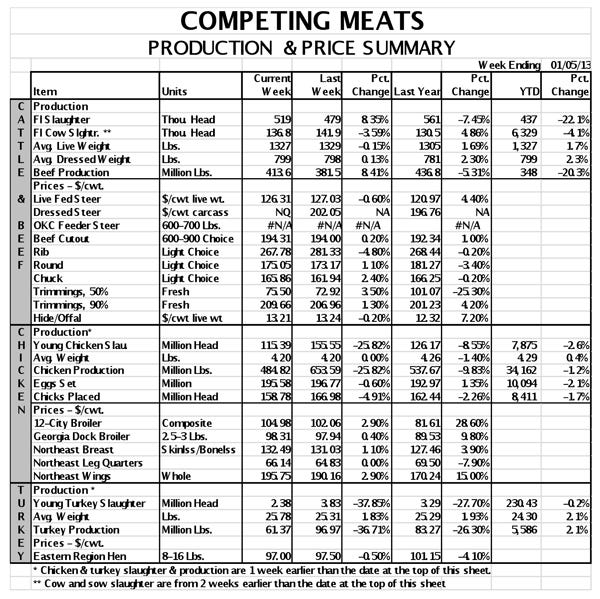

How high will beef prices rise? The Choice beef cutout finished the year at $194/cwt. and rose slightly last week. Figure 2 shows that feedlot placements since June have been far smaller than one year ago. The shortfall was over 10% in August, September and November, and nearly 20% in October. I still expect record-high beef prices at both wholesale and retail levels this year with the Choice cutout possibly exceeding $215/cwt. in the spring. Some say, “But consumers won’t pay that for beef.” Some won’t, I agree, but some will and the lower quantity that causes prices to increase will show up as lower consumption among beef consumers. What will they eat instead? It very well could be pork.

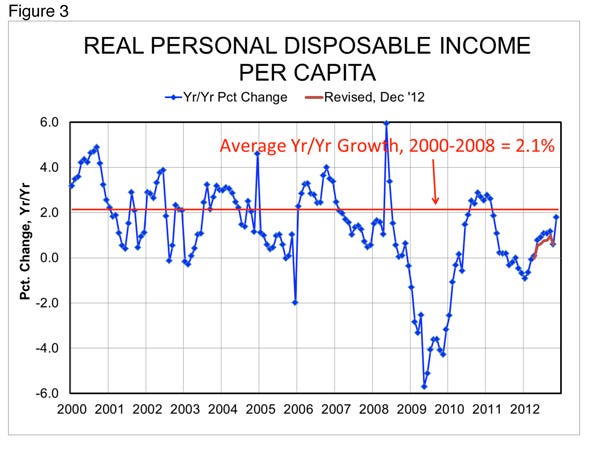

What will happen to consumers’ incomes? I saw a cartoon this morning that showed congress and the president jumping off the fiscal cliff only to land on a slightly lower ledge labeled, “Debt Ceiling Cliff.” Does anyone think the fiscal cliff issues are anywhere near resolved? I certainly don’t, and the uncertainty continues to cause businesses to balk at the long-term decisions that are needed to get the economy growing. That means putting people back to work, improving the quality of the jobs available and the support needed for robust consumer demand. Let’s all say it together: “Uncertainty makes people hesitate.” It is clear from Figure 3 that real personal disposable income per capita is not growing nearly as quickly as it once was. This is the take-home-pay variable of macro-economics. November’s 1.8% year-on-year growth was very encouraging, but it was accompanied by a set of downward revisions reaching back to January. Such negative revisions have been the norm for the past two years. I’m guessing the 1.8% will not survive, but I would take anything above 1% as a positive. The news is still not encouraging for this key measure of consumers’ abilities to buy goods and services, including meat and restaurant meals!

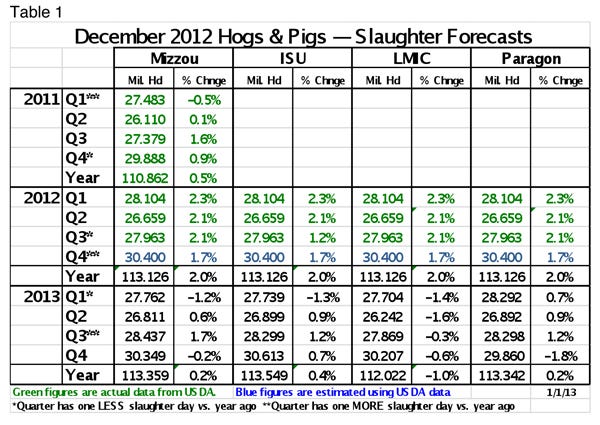

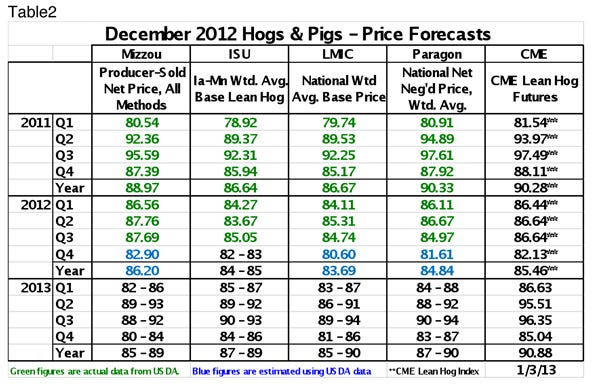

Will USDA’s December Hogs and Pigs report prove accurate? Hog supplies still matter and the report was a bit of a surprise to many. Hog producers have weathered the high feed-price storm better than expected and it appears that 2013 slaughter will be very close to 2012 levels. Slaughter forecasts from University of Missouri, Iowa State University, Livestock Marketing Information Center and Paragon Economics (me) appear in Table 1. Potentially lower weights (at least during the first half of the year), higher exports and population growth mean that stable slaughter will reduce per capita pork availability and push prices somewhat higher. Price forecasts appear in Table 2.

Regardless of what the year brings, I am reminded of the comment of a Republican friend the morning after the November election. He wisely noted, “God is still in His heaven and the Republic will survive.” Whether you share his sentiment about the Republic because of, or in spite of, the election is up to you, but I think the first part is as true today as it has been for eons and I find great solace in that. I hope you do, too. Many prayers and best wishes to you all for 2013!

You May Also Like

Enter a zip code to see the weather conditions for a different location.