Subscribe to Our Newsletters

National Hog Farmer is the source for hog production, management and market news

The events of the past six months, with huge swings in both hog markets and input costs have reinforced the volatility pork producers face nearly every day. As lenders and consultants, we have continually pushed the need for managing these price risks, but we also emphasize the need for business and estate planning.

November 26, 2012

The events of the past six months, with huge swings in both hog markets and input costs have reinforced the volatility pork producers face nearly every day. As lenders and consultants, we have continually pushed the need for managing these price risks, but we also emphasize the need for business and estate planning.

The unfortunate passing of Bob Christensen (Christensen Family Farms, Sleepy Eye, MN) a few weeks ago, undoubtedly led some producers to think about their own businesses and how they would move on if something were to happen to a vital member of their organization. Many have taken the basic steps for estate and tax planning, but it is important to think about how your plans are integrated into your business and the steps needed to get where you want to be.

Recently, I made presentation on exit strategies for those in the swine industry. My presentation did not just focus on exiting the business, per se, but rather addressed the long-term need to plan for the transition of a company. It seems that many producers operate as if their business will go on forever and they give little thought to the next steps until later in their business’ life cycle. I challenge young producers to begin thinking about transition and succession planning. The sooner you begin this process, the more solid and workable the plan will likely be.

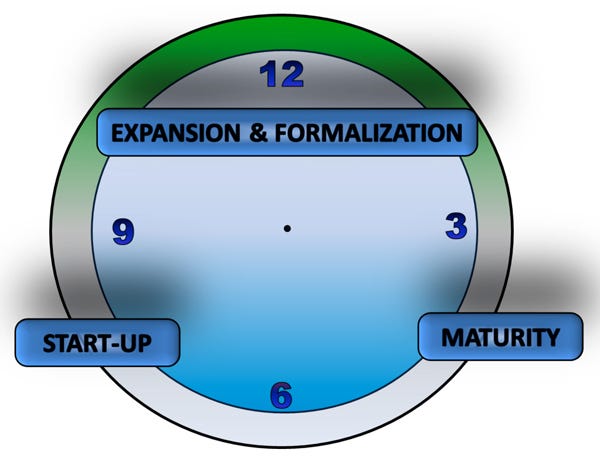

Conversely, during a transition to the next generation, older family members may not fully understand the changing family dynamics and the impact it can have on their business model. The graphic below, developed by our business consulting team, is a basic illustration of a business life cycle.

We have found that it helps clients think about where they are and it helps start the conversation about what the next steps should be. This simple graphic, comparing the life cycle of a business to a clock is meant to stimulate thoughts about how an organization may act through each stage without even knowing it.

An example would be the older generation of a farm family landing in the mature stage of the cycle while the younger generation is in startup or expansion stage. Each party can have vastly different views of where their business is going and what types of investments should be made. If this process does nothing more than get the parties to think from the other’s viewpoint for a short period of time, it can still be very helpful.

No doubt, transition and estate planning may not be the most exciting or cheapest experience in the world. In fact, some people would say they’re down right scared to open up a Pandora’s Box of family issues. But the earlier you begin this process, the better off you will be.

As a lender, I’ve had the opportunity to participate in or observe several transition programs. In almost all cases, these experiences helped strengthen the business model and flush out everyone’s longer term goals and desires. The important thing to note is that when you go through transition and estate planning, you are initiating another form of risk management. Done right, this process does not involve adjustments for tax planning, but it does give a producer a roadmap to follow so they can successfully transfer their business while still maintaining some liquidity for themselves without destroying family ties.

The first step in transition planning is identifying the needs and goals of all parties concerned. Then, the question comes down to finding the right parties to help in the process. There is an array of consultants available to help. Many have a wealth of knowledge and experience to help with both the “soft,” emotional side as well as the business and financial planning side of a transition plan. Having a consultant that can help manage all aspects of the transition plan, not just legal issues, will help lay the groundwork for success.

You May Also Like

Current Conditions for

50°F

Mostly Cloudy

Day 56º

Night 48º

Enter a zip code to see the weather conditions for a different location.