Subscribe to Our Newsletters

National Hog Farmer is the source for hog production, management and market news

July 29, 2013

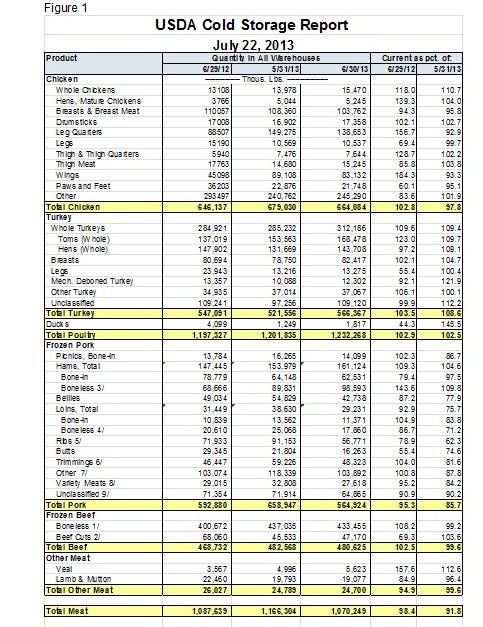

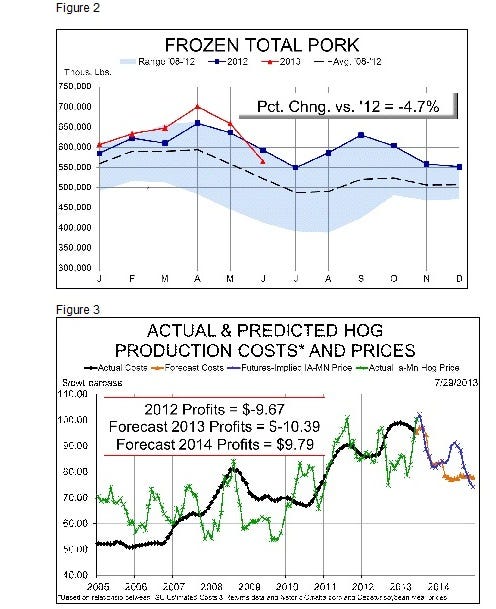

Total pork inventories as of June 30 were 4.7% lower than last year but remained just over 8% larger than the average of the past five years. That was a major feature of last week’s Cold Storage report from USDA. The data for all meat and poultry species appear in Figure 1.

Pork stocks normally fall in June as hog numbers decline but this year’s June drawdown was extraordinary. In fact, it was the largest June decline in frozen pork stocks in 20 years. The decline occurred even though ham stocks, which usually account for more than one-fourth of all pork in freezers, actually grew from their May 31 level. Ham stocks have, as usual, increased steadily since April but are now 9.3% larger than one year ago, and more than 27% larger than the average of the last five years.

Record belly prices in June drew a large number of bellies out of freezers, resulting in a sharp reduction of inventories. June 30 stocks were pegged at 42.7 million pounds, 22% lower than at the end of May and nearly 13% lower than one year ago. With prices at all-time record highs and given the seasonal tendency for belly prices to fall sharply come September, belly owners sold while the selling was good in June.

And there was good news for a rather troublesome pork cut over the past two years: ribs. Rib inventories grew sharply last year, creating a backlog of product that simply was not moving until this summer. Rib inventories fell nearly 38% in June to 56.8 million pounds. That figure is 21% lower than one year ago.

Like what you’re reading? Subscribe to the National Hog Farmer Weekly Preview newsletter and get the latest news delivered right to your inbox every week!

Pork trimmings prices have been at record-high levels as well, and trimmings inventories fell 18% in June. The 48.3 million pounds in freezers at month’s end were still 4% larger than last year and 5% higher than the five-year average. Continued high trim values could push stock significantly lower in July.

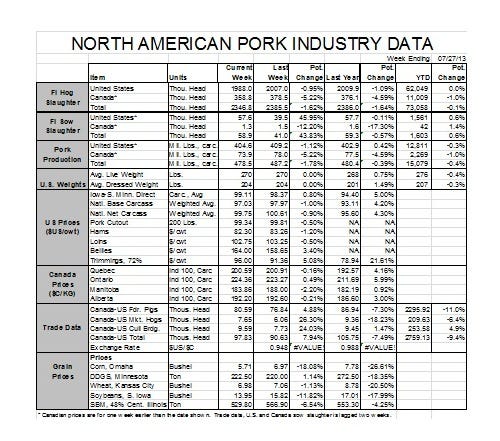

Last week was a good week for potential costs of production. Based on CME Group futures prices, projected costs for 2014 fell to $78.90 last week. The late week selloff in Lean Hogs futures kept forecast profit margins below $10 but the $9.79 per head figure as of this writing is vastly better than this year’s current projection of losses of $10.39 per head.

The entire trade will be looking forward to USDA’s August World Supply and Demand Estimates report, which will include this year’s first yield estimates based on actual data. Crop conditions improved last week and have some analysts now expecting a national average corn yield near 160 bushels per acre. Good news indeed!

You might also like:

Cases of Porcine Epidemic Diarrhea Virus Rise

You May Also Like

Enter a zip code to see the weather conditions for a different location.